|

My newsletter has a whole new look and lots of great information! I now have links to upcoming events as well as more customized searches. Check it out! Newsletter Highlights:

0 Comments

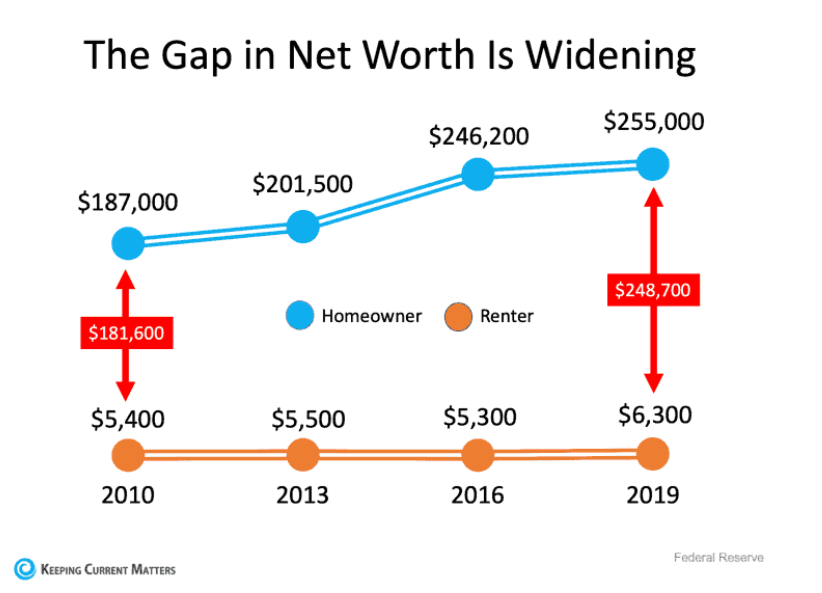

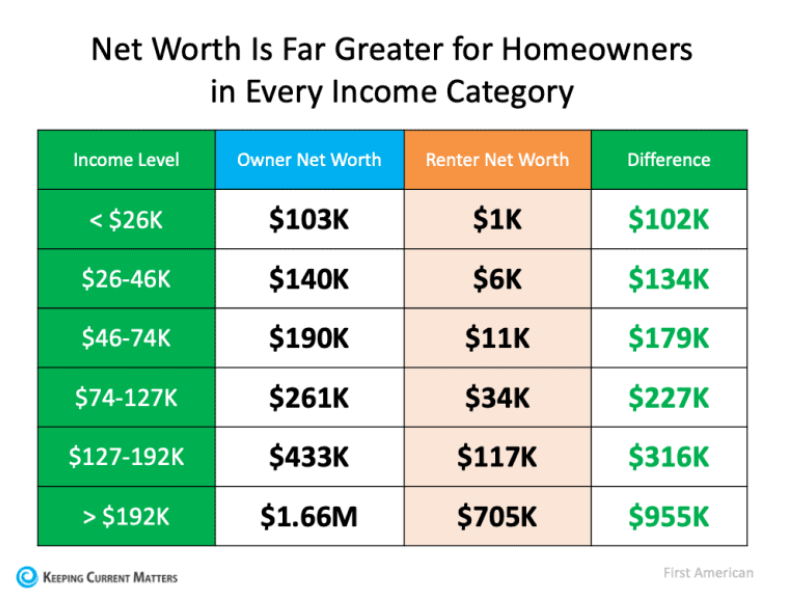

A Fannie Mae survey recently revealed some of the most highly-rated benefits of homeownership, which continue to be key drivers in today’s power-packed housing market. Here are the top four financial benefits of owning a home according to consumer respondents: · 88% – a better chance of saving for retirement · 87% – the best investment plan · 85% – the chance to be better off financially · 85% – the chance to build up wealth Additional financial advantages of homeownership included in the survey are having the best overall tax situation and being able to live within your budget. Does homeownership actually give you a better chance to build wealth? No one can question a person’s unique feelings about the importance of homeownership. However, it’s fair to ask if the numbers justify homeownership as a financial asset. Last fall, the Federal Reserve released the Survey of Consumer Finances, a report done every three years, with the latest edition covering through 2019. Their findings confirmed that homeownership is a clear financial benefit. The survey found that homeowners have forty times higher net worth than renters ($255,000 for homeowners compared to $6,300 for renters). The difference in net worth between homeowners and renters has continued to grow. Here’s a graph showing the results of the last four Fed surveys:  The above graph only includes data through 2019, but according to CoreLogic, the equity held by homeowners grew by $26,300 over the last twelve months alone. That means the gap between the net worth of homeowners and renters has probably widened even further over the last year. Some might argue the difference in net worth may be due to homeowners normally having larger incomes than renters and therefore the ability to save more money. However, a study by First American shows homeowners have greater net worth than renters regardless of their income level. Here are the findings:  Others may think homeowners are older and that’s why they have a greater net worth. However, a Joint Center for Housing Studies of Harvard University report on homeowners and renters over the age of 65 reveals:

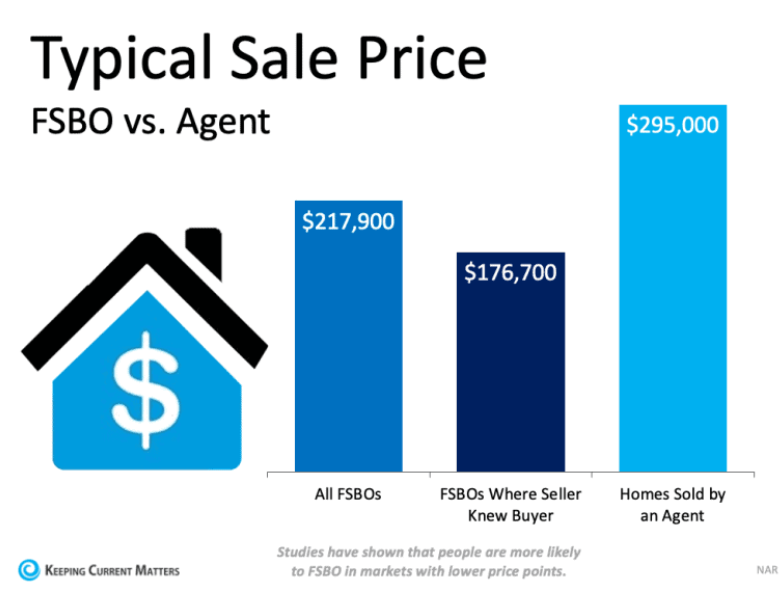

“The ability to build equity puts homeowners far ahead of renters in terms of household wealth…the median owner age 65 and over had home equity of $143,500 and net wealth of $319,200. By comparison, the net wealth of the same-age renter was just $6,700.” Homeowners 65 and older have 47.6 times greater net worth than renters. Bottom Line The idea of homeownership as a direct way to build your net worth has met the test of time. Contact a local real estate professional if you’re ready to take steps toward becoming a homeowner. www.keepingcurrentmatters.com  In a sellers’ market, some homeowners might be tempted to try to sell their house on their own (known as For Sale By Owner, or FSBO) instead of working with a trusted real estate professional. When the inventory of homes for sale is as low as it is today, buyers are eager to snatch up virtually any house that comes to market. This makes it even more tempting to FSBO. As a result, some sellers think selling their house will be a breeze and see today’s market as an opportunity to FSBO. Let’s unpack why that’s a big mistake and may actually cost you more in the long run. According to the Profile of Home Buyers and Sellers published by the National Association of Realtors (NAR), 41% of homeowners who tried to sell their house as a FSBO did so to avoid paying a commission or fee. In reality, even in a sellers’ market, selling on your own likely means you’ll net a lower profit than when you sell with the help of an agent. The NAR report explains: “FSBOs typically sell for less than the selling price of other homes; FSBO homes sold at a median of $217,900 in 2020 (up from $200,000 in 2019), and still far lower than the median selling price of all homes at $242,300. Agent-assisted homes sold for a median of $295,000…Sellers who began as a FSBO, then ended up working with an agent, received 98 percent of the asking price, but had to reduce their price the most before arriving at a final listing price.” When the seller knew the buyer, that amount was even lower, coming in at $176,700 (See graph below):  That’s a lot of money to risk losing when you FSBO – far more than what you’d save on commission or other fees. Despite the advantages sellers have in today’s market, it’s still crucial to have the support of an expert to guide you through the process. Real estate professionals are trained negotiators with a ton of housing market insights that average homeowners may never have. An agent’s expertise can alleviate much of the stress of selling your house and help you close the best possible deal when you do.

Bottom Line If you’re ready to sell your house this year and you’re considering doing so on your own, be sure to think through that decision carefully. Odds are, you stand to gain the most by working with a knowledgeable and experienced real estate agent. Contact a local professional to learn more about how a trusted advisor can help you, especially in today’s market. www.keepingcurrentmatters.com Newsletter Highlights:

For generations, the homebuying process never really changed. The seller would try to estimate the market value of the home and tack on a little extra to give themselves some negotiating room. That figure would become the listing price of the house. Buyers would then try to determine how much less than the full price they could offer and still get the home. The asking price was generally the ceiling of the negotiation. The actual sales price would almost always be somewhat lower than the list price. It was unthinkable to pay more than what the seller was asking.

Today is different. The record-low supply of homes for sale coupled with very strong buyer demand is leading to a rise in bidding wars on many homes. Because of this, homes today often sell for more than the list price. In some cases, they sell for a lot more. According to the Home Buyers and Sellers Generational Trends report just released by the National Association of Realtors (NAR), 45% of buyers paid full price or more. You may need to change the way you look at the asking price of a home. In this market, you likely can’t shop for a home with the old-school mentality of refusing to pay full price or more for a house. Because of the shortage of inventory of houses for sale, many homes are actually being offered in an auction-like atmosphere in which the highest bidder wins the home. In an actual auction, the seller of an item agrees to take the highest bid, and many sellers set a reserve price on the item they’re selling. A reserve price is the minimum amount a seller will accept as the winning bid. When navigating a competitive housing market, think of the list price of the house as the reserve price at an auction. It’s the minimum the seller will accept in many cases. Today, the asking price is often becoming the floor of the negotiation rather than the ceiling. Therefore, if you really love a home, know that it may ultimately sell for more than the sellers are asking. So, as you’re navigating the homebuying process, make sure you know your budget, know what you can afford, and work with a trusted advisor who can help you make all the right moves as you buy a home. Bottom Line Someone who’s more familiar with the housing market of the past than that of today may think offering more for a home than the listing price is foolish. However, frequent and competitive bidding wars are creating an auction-like atmosphere in many real estate transactions. For the best advice on how to make a competitive offer on a home, reach out to a local real estate professional who’s an expert in your local market. www.keepingcurrentmatters.com Newsletter Highlights

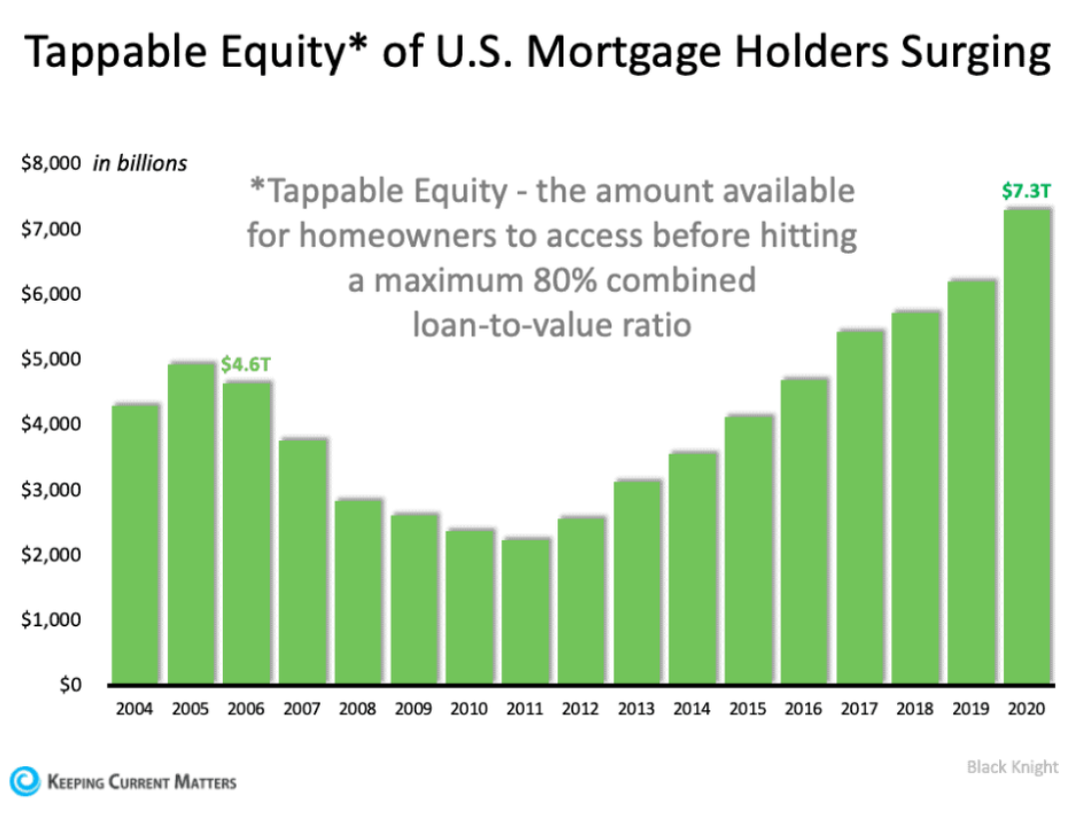

Freddie Mac recently released their Quarterly Refinance Statistics report which covers refinances through 2020. The report explains that the dollar amount of cash-out refinances was greater in 2020 than in recent years. A cash-out refinance, as defined by Investopia, is: “a mortgage refinancing option in which an old mortgage is replaced for a new one with a larger amount than owed on the previously existing loan, helping borrowers use their home mortgage to get some cash.” The Freddie Mac report led to articles like the one published by The Real Deal titled, House or ATM? Cash-Out Refinances Spiked in 2020, which reports: “Americans treated their homes like ATMs last year, withdrawing $152.7 billion amid a cash-out refinancing spree not seen since before the 2008 financial crisis.” Whenever you combine the terms “spiked,” “homes like ATMs,” and “financial crisis,” it conjures up memories of the housing crash we experienced in 2008. However, that comparison is invalid for three reasons: 1. Americans are sitting on much more home equity today. Mortgage data giant Black Knight just issued information on the amount of tappable equity U.S. homeowners with a mortgage have. Tappable equity is the amount of equity available for homeowners to use and still have 20% equity in their home. Here’s a graph showing the findings from their report:  In 2006, directly before the crash, tappable home equity in the U.S. topped out at $4.6 trillion. Today, that number is $7.3 trillion. As Black Knight explains: “At year’s end, some 46 million homeowners held a total $7.3 trillion in tappable equity, the largest amount ever recorded…That’s an increase of more than $1.1 trillion (+18%) since the end of 2019, the largest percentage gain since 2013 and – you guessed it – the largest dollar value gain in history, to boot. All in all, it works out to roughly $158,000 on average per homeowner with tappable equity, up nearly $19,000 from the end of 2019.” 2. Homeowners cashed-out a much smaller amount this time. In 2006, Americans cashed-out a total of $321 billion. In 2020, that number was less than half, totaling $153 billion. The $321 billion made up 7% of the total tappable equity in the country in 2006. On the other hand, the $153 billion made up only 2% of the total tappable equity last year. 3. Fewer homeowners tapped their equity in 2020 than in 2006. Freddie Mac reports that 89% of refinances in 2006 were cash-out refinances. Last year, that number was less than half at 33%. As a percentage of those who refinanced, many more Americans lowered their equity position fifteen years ago as compared to last year. Bottom Line It’s true that many Americans liquidated a portion of the equity in their homes last year for various reasons. However, less than half of them tapped their equity compared to 2006, and they cashed-out less than one-third of that available equity. Today’s cash-out refinance situation bears no resemblance to the situation that preceded the housing crash. Newsletter Highlights:

I am proud to be named one of the Top 50 New Hampshire Real Estate Agents On Social Media! This award is super special to me because the proper marketing of your property is crucial when selling your home. I pride myself on utilizing various marketing techniques to highlight my clients property to provide them with the best exposure to potential buyers (ESPECIALLY social media!) Read the full article by clicking on the image below:  |